As shipping freight rates fall; what does the future hold?

What is the

similarity between oil prices and shipping freight rates? Of course, the first

similarity is that the prices of oil and shipping freight rates have been

consistently falling for the last two years. Both oil prices and shipping

freight have another similarity. Both have been hit by a global economic

slowdown which has resulted in contraction in demand. But the most important

similarity between oil prices and shipping freight rates has been the build-up

of excess supply. Like oil companies invested heavily in shale capacity when

oil prices were at above $100/bbl, similarly shipping companies also built up

tremendous capacities during the last 3 years when the CCFI Freight Index was

quoting in the range of 1150-1200. Today the index is down to 735 and, with

more capacity coming up by the year 2019 it is doubtful how much the freight

rates can increase from here.

Consider this

simple example. Today it costs less than $300 to move a 40-foot container from

Shenzhen in China to Rotterdam in the Netherlands. This is not even sufficient

to cover the cost of fuel and handling. Even if we do not consider the

exorbitant Suez Canal fees, the entire trip is unviable to begin with. But

cargo is still moving at these cheap rates, before ships cannot afford to idle.

Remember, both oil extractors and shipping companies have taken on tremendous

debt to fund this expansion and hence they will have to continue to supply,

irrespective of low prices.

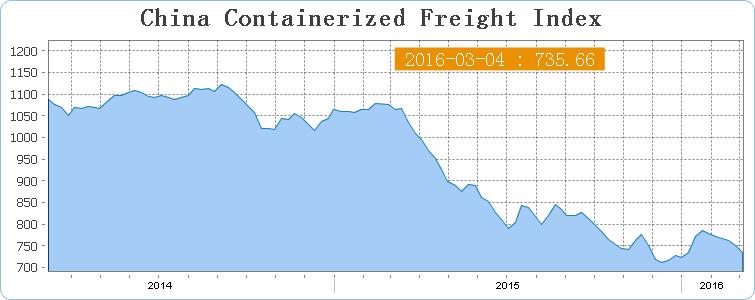

Falling Freight Index...

As the above

chart suggests, Shipping Freight Index has fallen from a high of 1150 in 2014

to as low as 735 in March 2016. For a very long time, the large shipping

companies could manage to maintain the price at profitable levels due to their

control over the shipping lines. But then, enormous shipping capacity has been

built up in the last 3 years. Shipping capacity grew from 15.4 million TEU in

2011 to 19.6 million TEU in 2015. Hence, the luxury of managing price is not

there with shipping companies any longer. The immediate mandate is to run all

ships at full capacity and focus on market share instead of pricing.

So, is it all about a global slowdown in trade?

There has

been a slowdown in trade worldwide over the last one year, including in China.

But weak trade does not tell the whole story. For example, China’s annual

imports are at $1.95 trillion and annual exports at $2.4 trillion. At a total

trade value of $4.35 trillion, China is still contributing a lot more to global

trade than it was doing 3 years ago. Ironically, the CCFI freight index was at

a high of 1200 before 3 years. Therefore, the fall in volumes does not entirely

explain the sharp fall in shipping freight rates.

It is actually about overcapacity in shipping:

We have

already seen how Global Container Ship Fleet has increased its capacity by 27%

in the last 4 years. The demand has simply refused to keep pace with this

massive overcapacity that was initiated back when the CCFI Freight Index was at

a high of 1150-1200 range. In fact, global consultancy firms like the Boston

Consulting Group (BCG) expect another 30% increase in container ship fleet

capacity by 2019 before the overall supply will plateau out.

The road ahead for container ships:

The scenario

described above is hardly a sustainable scenario. But the bottom-line is that

this situation is unlikely to change for the next couple of years till the time

supply does not plateau and demand does not pick up. Both are unlikely to

happen immediately. Broadly, there are a few key strategies that global

shipping freight companies are adopting to overcome this supply glut:

·

The fist strategy has been to keep their cost of

operation at optimal levels to stem losses for the next few quarters. One

example is of container ships moving oil via the Cape of Good Hope instead of

the Suez Canal. Due to cheap crude oil prices, shipping companies can afford to

do the same. This also enables them to save on the Suez Canal fees and also

make profit out of trading in oil in the midst of volatile prices.

·

Some shipping companies are trying to kill

excess capacity to ensure that this supply disruption will impact prices

positively. For example, Maersk A/S, the world’s largest shipping company has

recently cancelled orders for 6 Triple-E class ships. Such cancellations may

become more common as shipping fleets will try to move towards supply

disruption.

·

Shipping of freight is a highly commoditized

business and the scope for differentiation is quite limited. Hence some of the

larger shipping fleets are trying to diversify towards other higher margin

businesses like port terminal operations, marine maintenance services and

supply chain management.

·

There is likely to be a major shakeout in the

shipping freight industry. Many large fleets have invested hugely in creating

economies of scale. Smaller and medium sized companies in this space may now

become acquisition targets as supply gets automatically streamlined and

rationalized. Normally, such tough times get to see synergistic alliances where

competitors tend to complement each other. For example, two of the largest

shipping companies, Maersk A/S and MSC have already formed alliances to share

routes and costs. Similarly, four of the largest Chinese have also formed a

national alliance to create virtual scale in the shipping industry to tide over

this situation.

Future lies in Uberization of Shipping Fleet:

We believe

that the future of the Shipping freight industry lies in a kind of Uberization.

Today the Shipping industry is vastly demarcated between the large fleet

carriers and the small & medium sized carriers. The small and medium

carriers are already finding it hard to survive in this tight freight market.

With the larger names forming formal and informal alliances, the effort will be

to squeeze out the small and mid-sized companies from the shipping freight

business. The major drawback in the global shipping freight industry is that

there is no scientific methodology for aggregating demand and supply and

matching them. Once this is done the entire shipping freight business can

become a lot more democratic and competitive. That is probably the best answer

to the woes of the shipping freight industry today.

China Freight give shipping organization, my business relies upon the an extensive variety of shipping basically China to USA, Canada, UK, Australia. Genuinely It is a trying occupation to shipping things to other places,shipping to USA from China by means of sea. So China Freight offers a gave FBA transport advantage for brisk with safe movement. For More Info:- Shipping from China to USA

ReplyDeleteGreat article! If anyone looking for the Sea Freight Philippines feel free to ask me.

ReplyDelete